A look back to 2025…

Global markets delivered solid gains in 2025 despite a year marked by political drama, shifting interest rate expectations and ongoing geopolitical tension. While frequent bouts of volatility were unnerving, the patient investor who stayed the course was rewarded as both equities and bonds ended the year up overall.

The prevailing topic of 2025, by Q4 speculation regarding a potential AI bubble reached fever pitch. While some air has since been let out of the valuation balloon and the bubble narrative has moderated somewhat, we remain vigilant to the risk this sector still poses. Given the current velocity of the AI related buildout, it appears that investment will continue at pace for a while yet.

As we enter 2026, our investment outlook is positive while we recognise and continuously monitor the shifting sands of the geopolitical backdrop. It will be an interesting year given the current rate of technological change, the upcoming US mid-term elections and ongoing recovery in select economies – New Zealand included. While there are always risks to investing and competing economic headwinds will doubtless bring some turbulence, the backdrop to corporate profitability appears healthy and supportive.

Kind regards,

Tim Chesterfield

Chief Investment Officer Perpetual Guardian Investments

Fixed income, currencies and alternatives

With equity investments proving somewhat volatile, fixed income (bonds) provided a useful counterbalance, with New Zealand bonds returning 5.5% and global bonds (hedged) 3.7% over the year. Short-term cash returned 3.6%, highlighting the benefit of holding longer-dated bonds for those seeking an income stream that keeps pace with rising prices.

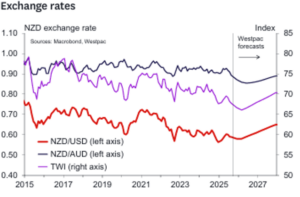

The New Zealand dollar was broadly steady over the final quarter but weaker over the year, particularly against the euro and Australian dollar, giving an extra lift to offshore investment returns. Alternative assets also delivered positive results despite some concerns emerging in private credit where signs of stress emerged. Private credit has seen significant growth and whilst the yields attainable are attractive this is to reward investors for the increased risk of holding such investments.

The New Zealand dollar was broadly steady over the final quarter but weaker over the year, particularly against the euro and Australian dollar, giving an extra lift to offshore investment returns. Alternative assets also delivered positive results despite some concerns emerging in private credit where signs of stress emerged. Private credit has seen significant growth and whilst the yields attainable are attractive this is to reward investors for the increased risk of holding such investments.

New Zealand

New Zealand equities advanced 3.3% for the year and 1.9% over the final quarter, lagging overseas markets but showing signs that we may be past the malaise of the recent economic downturn. Recent company announcements have showed early signs of improvement, with larger, higher-quality companies delivering better results and more hopeful outlooks.

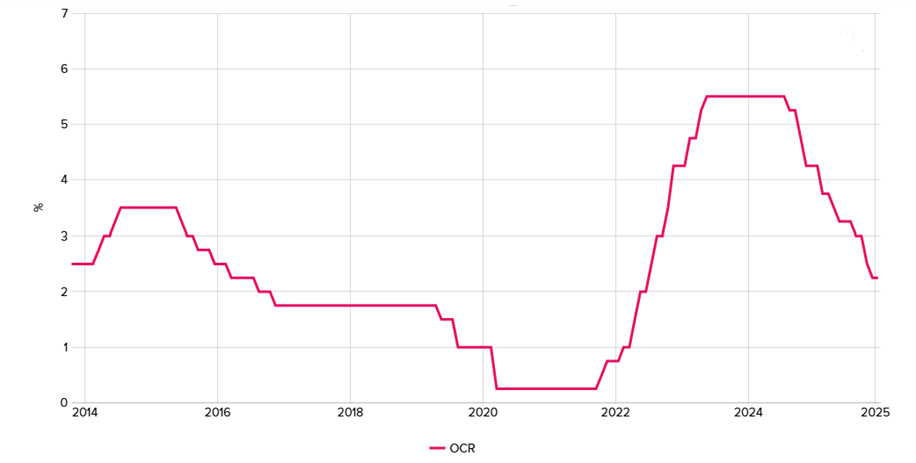

Looking into 2026, the official cash rate (OCR) is now close to the bottom of the cycle at 2.25%, which should start to support household finances in the first half of the year. With an election approaching and fiscal policy likely to be more supportive, more reasonable valuations on an income basis, leads us to be hopeful that New Zealand companies enter the year on a more constructive footing.

New Zealand property

Listed property was strong in 2025, returning 12.7% as falling interest rates supported the sector, although momentum faded late in the year and the index fell 4.0% over the final quarter. Many property companies still trade at discounts to the value of their underlying assets, which may lead to further optimism should conditions continue to improve.

With high levels of debt, generally above 30%, the move lower in interest costs can have a meaningful impact on profitability as they decline. As confidence returns, more equity raisings should be expected, where companies look to fund new growth opportunities. This presents a double-edged sword with companies likely issuing a mix of equity and debt, which will present investors with calls to invest married with the opportunities for long-term growth. Not all projects will be created equal.

Australia

Australian shares finished the year up 16.0% in New Zealand dollar terms, but the December quarter was softer, with equities down 0.8% in Australian dollars (up 0.9% for New Zealand investors). Sentiment turned after inflation surprised on the upside at 3.8% and the Reserve Bank of Australia shifted from an easing bias to a slightly more hawkish stance, increasing the risk of a rate rise in 2026.

Despite this, the three interest rate cuts delivered in 2025 have yet to fully filter through to households, where spending has remained resilient. Together with supportive fiscal policy, this should help underpin economic growth for 2026, even as markets adjust to the possibility of higher-for-longer interest rates than previously assumed.

International

Global equities rose 19.6% in New Zealand dollar terms over 2025, helped by steady economic growth and resilient company earnings. Europe, emerging markets, the UK and Japan all rose strongly with Europe up 32.3%, emerging markets 30.8%, the UK 26.9% and Japan 22.7%, while the US gained a more modest but still positive 13.3%.

Within this, artificial intelligence was a standout theme, driving strong gains in technology companies in the US, Japan and parts of Asia. Emerging markets benefited from a weaker US dollar and robust earnings from Taiwan and South Korea, while European markets were lifted by strength in basic resources, banks and healthcare, alongside a more reassuring fiscal outlook in the UK.